Unboxing Intra- African Payments: Why Payments is fragmented in Africa.

Unboxing Intra- African Payments: Why Payments is fragmented in Africa.

plus what Banks, Fintechs and Regulators are doing in 2023 | Vol 36| Aug 15th, 2023

Long but insightful read alert🍿

Picture this:

You live in Africa and you want to buy a box of aromatic coffee beans from Ethiopia or quality leather from Northern Nigeria. You finally locate a Seller and you want to make Payments. These are likely scenarios that could play out:

You will be unable to buy the item because the Seller can’t receive Payments from you.

You will be able to make the Payments but the Seller will receive it in a couple of days.

The Payment will be more expensive than buying from Amazon or Ebay.

You might need to travel to that country with cash to physically buy the goods and travel back.

The above☝🏽my friends, is the problem of Payments fragmentation in Intra African trade. We’ll review this in this edition, and take it up a notch by exploring what African stakeholders are doing in 2023 to reduce the gap.

Before we jump in, these are some terms we will be coming across quite often in this piece.

📌RTGS: An Real Time Gross Settlement System that is used mainly for large value and important funds settlement instructions to be processed within a payment system in one country.

📌FMI: Financial market infrastructures refer to all parts of the financial system that facilitate financial market transactions e.g clearing and Settlement systems.

📌Correspondent Bank: It is a financial institution that provides services to another one—usually in another country. It acts as a proxy guaranteeing and facilitating payments.

📌Remittance: Cross-border payments are financial transactions where the payer and the recipient are based in separate countries.

The Genesis: Africa is not a Country.

To understand the fragmentation you need to understand Africa. We have always said that Africa is not a country, but Africa is also not a normal continent.

With about 54 countries, 42 currencies, over 1.4 billion people, over 2,000 languages, 6 political zones, and 8 Regional economic communities.. nah. Africa is not your usual continent.

Many Fintechs who have entered the continent with an African Strategy had to beat a hasty retreat, and it’s not because of the mosquitoes or spicy food.

It’s because having one African Strategy will simply not work.

The effects of Money flow.

So what really happens when you try and send money from Nigeria to Ethiopia?

It’s shocking, but that money first travels to some bank in North America, before it travels after some days to a bank in Ethiopia and then- gets to the seller.

But why? Because Banks in Nigeria and Ethiopia have no direct way of clearing and settling the payment. So they use correspondent banks (defined above) and most are located in the US and Europe. This diagram by Glenbrook explains it well.

Some stats: More than 80% of the transactions sent from Africa to a corresponding bank in the US have their final beneficiary in another Country.

Of that figure, 19.5% are headed back to a Bank in Africa and 54% are headed to a bank in Asia. Now you know why importing from China isn’t straight-forward 🤔

The Architecture of Regional Payments

Ok enough about the problem, we now understand it.

What has been done since then to solve it? 🤔

The best way to innovate away from fragmentation is to innovate within each fragmented piece. This is where we focus on the regional payment infrastructure. A study by SWIFT showed that Intra-region policies in the SADC and UEMOA reduced their dependence on dollar remittance and also increased intra-region trade.

For more banks to collaborate with themselves, FMIs( see above) need to be in place. If we are to solve a Settlement problem then we need to have more National and Regional Switches and Settlement systems. These are a few of the operational infrastructures.

BEACO: The BEACO Is the central bank of the 8 states in the WAMU region.

EAPS: The East African Payment System links all the national settlement systems in the EAC region using the SWIFT system as RTGS.

SIRESS( has been renamed): The SIRESS is an automated interbank settlement system operated by the SARB, as appointed by the participating SADC central banks, to settle their obligations and payments on an immediate, real-time basis in the region.

Ok so you’ve seen some progress, but it is Bank-heavy right?, what about the Fintechs?

This is the thing yeah - for every Fintech who announces they have launched one snazzy cross-border product or partnership, there is a bank, national switch or regional switch that is doing the heavy lifting. OR they are using Crypto rails.

But still, a lot has been done on the Fintech front this year and we highlight just 6 of them in the infographic below.

Fast forward to 2023- The State of FMIs.

What of the Infrastructure? Since we know they are the building block for seamless affordable payments in Africa, what developments are happening?

Take a look at 10 investments, policies, and tech updates focused on developing payment infrastructure around Africa.

Sierra Leone: Sierra Leone launched their National Payment Switch last week. This was 12 years after the initial RFP. World Bank assisted this project with $12M USD.

South Africa: This year, SARB debuted a payment platform, PayShap which enables South Africans to make real-time payments using identifiers like mobile numbers or e-mail.

Sao tome n Principe: The government of São Tomé and Príncipe signed a $ 3.2 million loan agreement with the AFDB to upgrade the national switch payment system - RTGS and ACH functionality.

Kenya: The CBK upgraded the Kenya Electronic Payment and Settlement System to new global standards ISO 20022 to boost the processing of large-value transactions.

Liberia: The Central Bank of Liberia received a grant of $3.9 million from the AFDB for an upgrade to Liberia’s payments infrastructure and systems project.

South Sudan: The Bank of South Sudan has restricted the use of the US dollar in local transactions as it moves to de-dollarize the economy.

Somalia: The Central Bank of Somalia rolled out the use of IBAN by commercial banks. This will enhance processing through the National Payment System.

WAMZ: West African Monetary Institute Partners with EMTECH to Modernize Fintech Regulatory Frameworks Across the WAMZ.

China-Africa cross-border yuan settlement center opens in Yiwu to establish cross-border yuan settlement channels and explore interbank.

UEMOA : GIM-UEMOA migrates to ISO 20022 as it joins nexo standards to augment cross-border payments in West Africa

Focus on PAPSS

No discussion about trans-African payments in 2023 will be complete without discussing PAPSS.

The Pan-African Payment and Settlement System is a Pan-African real-time gross settlement (RTGS) infrastructure for cross-border payments in local currencies.

It was launched on January 13, 2022, and works in collaboration with Africa’s central banks to provide a payment and settlement service which connects Banks, payment service providers, and Fintechs across Africa.

Since then they have had slow but steady progress in tackling the challenge of onboarding and fine-tuning integrations across countries. From all we have discussed above, you’ll agree it isn’t going to be a walk in the park.

From our Insights Product, we have filtered info on their progress so far this 2023 in the infographic below.

Ideas for moving forward

We like to keep our newsletters brief ( hehe.. not this time), with just as many details to spark curiosity and a healthy debate. So everything we have written so far is not exhaustive on this subject. But we will end with some brief recommendations to build on the progress made.

Regional Payment Systems should be Interoperable. PAPSS is focused on this but other bodies can join in.

Also, Mobile money wallets should be Interoperable across countries and Schemes. M-PESA, Momo, Ecash , ZeePay, and Opay should get together and make magic.

The rise of Regional currencies will also help eliminate fragmentation.

Cash management and treasury operations are expensive, this is one of the value props of CBDC and Cryptocurrency. Many African governments are shifting their stance on the latter but more research and testing should be encouraged.

….and that is our piece! Thanks for making it here.

Now to something else.

🥸 Unpopular Opinion - Fintech Ops is a Profit center.

The Seamless Fintech Operations Course is back for the last time this year.

It is designed to provide you with practical knowledge and skills for operating Fintech products and rails.

We received awesome feedback from the last Cohort - check it out here.

By the end of the Seamless Fintech Operations Course,

You will have a deep understanding of the business of the Fintech you work for.

You will be able to identify bottlenecks in the operations process of your product.

You will also be able to identify parameters in your products that will make settlements efficient within your company and with your partners, among other things.

Resolve customer challenges proactively, protect your brand promise and maintain high confidence levels and much more.

Have any questions? Shoot us a mail at info@thepaymentlogue.com.

Registration is on at the moment. Join Fintech Founders and executives who now have better control of their operations overhead by building effective operations around their innovative Fintech platforms.

Classes are online, on Saturday, from 9 a.m. to 12 noon for 4 weeks. To learn more and download a detailed curriculum- click here:

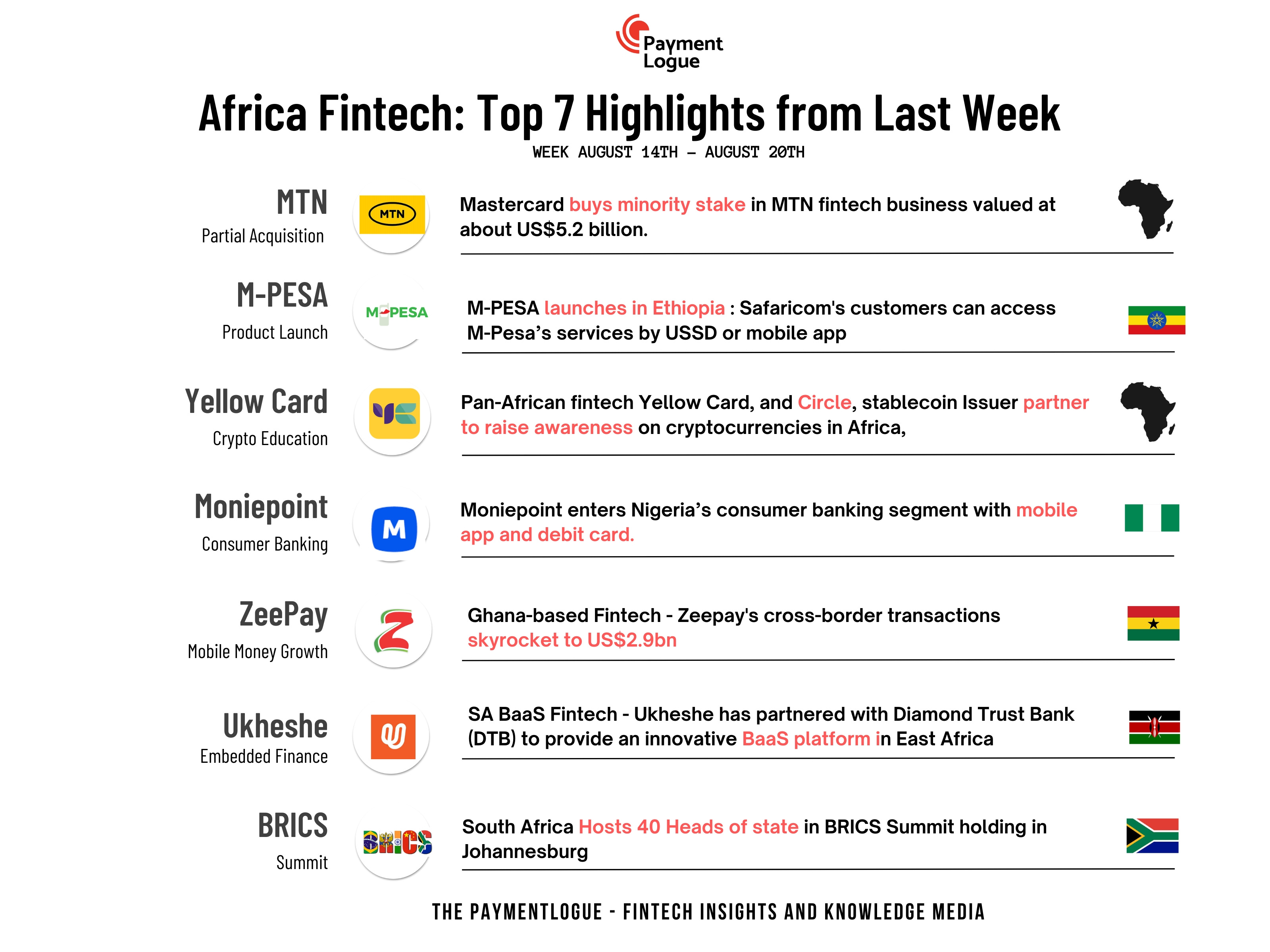

The Weekly Roundup

Many interesting things happened in the African Fintech scene last week; From Mastercard taking a chunk of MTN’s Fintech Business to M-PESA’s launch in Ethiopia, the continent was buzzing.

Catch up on 7 highlights we think you shouldn’t miss from last week’s news. Take a look 👇🏽.

And that is all for this week’s newsletter. Have an awesome week!

This is an educative read, thanks.