Fintechs in Financing - The New School of CreditTech 💹📅.

Fintechs in Financing - The New School of CreditTech 💹📅.

Why Sweat Equity as Collateral is winning in Africa| Vol 36| Aug 15th, 2023

Hello Fintech Friends,

It’s another Tuesday and a good time to get into the deets of African Fintech.

Shall we? Just before we jump in, we do our best to bring a detailed view of African Fintech each week. More eyes need to see this and you can help by subscribing, sharing, and engaging in the comments.

What do we have in this week’s dose of African Fintech 💊?

📌Reviewing the rise of Fintechs in Financing and why VCs love them💰

📌 How to join Fintech CEOs who have stopped micromanaging their staff 🔎

📌 As usual, The Weekly roundup in a shareable infographic.

🙃The New-ish world of Sweat Equity as Business Collateral.

Sweat equity is when Business owners use their time and effort to contribute to the success of a company. Traditionally Businesses use assets like land, deposits, and housing to get loans. When a business is just starting out, they can’t get funding the usual way because they do not qualify. And this is where alternative funding comes in

But why we are discussing this in August?….

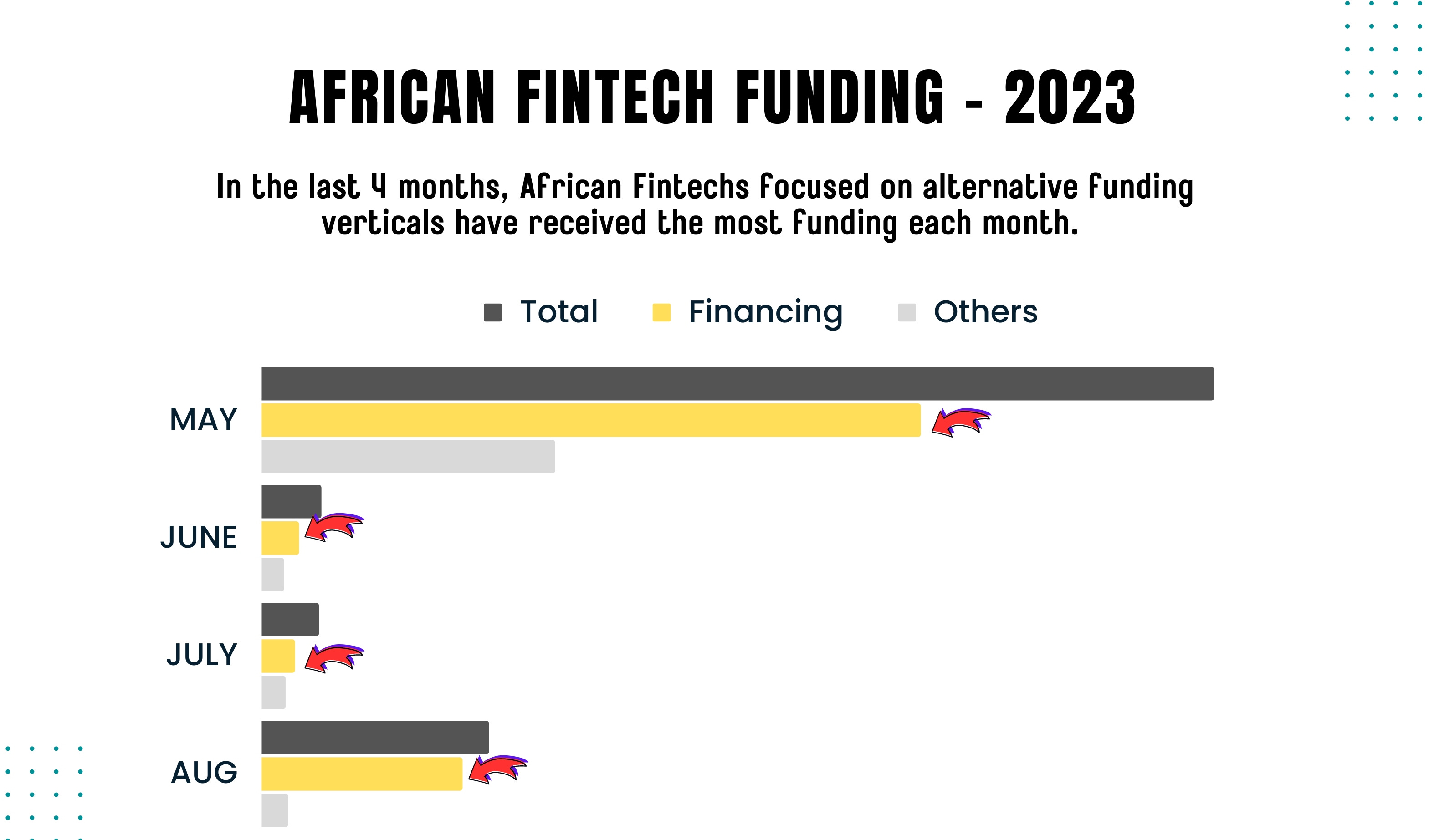

Moove raised almost $90m so far this year and $334m since Feb of 2022, M-KOPA raised a whopping $250M in May, and Yellow raised $14m in June all making it to the highest funded fintech for each of the months this year.

What is the common factor tying all these Fintechs together - alternative financing!

Some Definitions

Financing can mean the same thing as getting a loan, but it is different as it implies seeking money from a non-traditional source, such as an alternative financing company.

There are also differences when you consider factors like time and underwriting criteria.

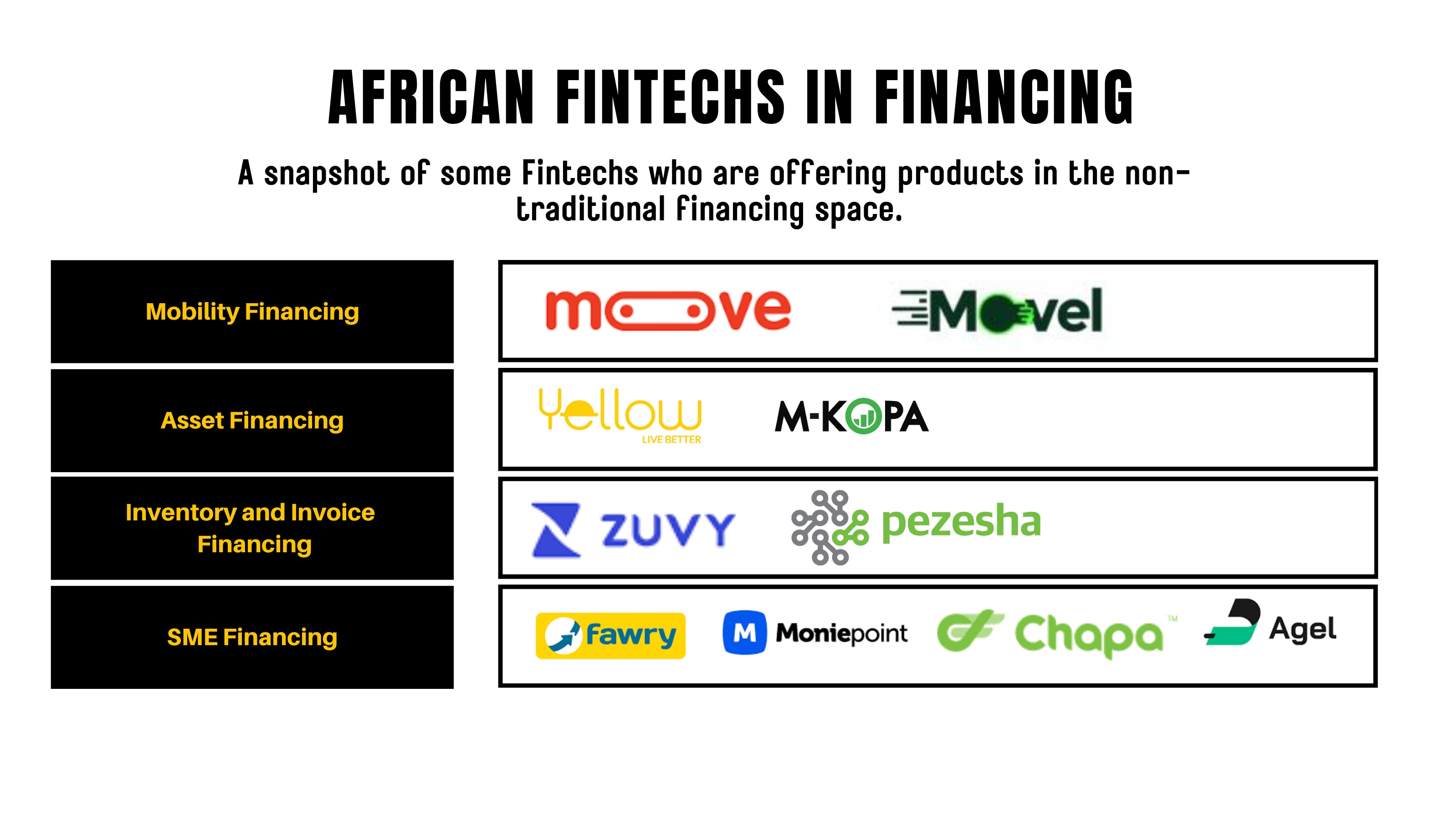

What are the common categories?

Asset Financing: Financing to get things like phones, energy devices etc.

SME Financing: General financing for SMEs based on different criteria.

Mobility Financing: Financing for transportation devices like cars and bikes.

Invoice Financing: Financing based on business the SME has done or has been awarded.

We say they give collateral based on sweat equity as it involves a lot of energy and effort on the SME’s part to fulfil the requirements of the finance for e.g. Moove and Uber deal for car financing for the drivers.

A snapshot of African Fintechs in these categories

Financing vs Loans

You might be wondering like I did - Why aren’t the SMEs taking loans and why aren’t the banks actively pursuing this space? 🤔

Banks prefer to extend loans to large corporates because credit history is easier to access, and the amount needed is large.

SMEs are in sectors with little collateral or in environments where contract enforcement is weak cos of a lack of identification.

The fixed cost of credit risk assessment to reduce the information asymmetry between SMEs and banks is too high, to push banks to finance SMEs without an element of subsidy.

As written in this insightful piece by benefactors.io

Ask any SME and they will likely tell you that they need financing but that they don’t take a bank loan to finance their business due to the cost of credit. At 16-18% annual interest rate plus fees and charges, only the most profitable companies can afford credit.

If you speak to the banks, they will tell you that SMEs are not “bankable”. The risks are too high and it’s not feasible to lower their interest rates and get a commercial return. Banks end up highly liquid and struggle to hit their own targets for SME lending.

What is the Opportunity?

It’s almost apparent from the above, but let’s break it into specifics to see how Fintechs add value. Technology becomes the game changer for Financial houses to offer this service to SMEs as they do for large corporates at worthwhile price points.

Specifically according to an FSD report, these are some FinTech credit innovations in Africa.

Scoretechs: Credit scoring platforms that allow for easier credit risk assessment of African SMEs. (Which Moove and M-KOPA use)

Invoicetechs: Digital invoice trading platforms for African SME working capital needs

Telco-based lenders: FinTech platforms that rely on data from mobile money transactions to make loans to African SMEs.

Pay as you go (PAYG): FinTech platforms that leverage on the assets being financed as collateral.

Fintechs partnering and innovating in the Financing space.

Kenya’s Pezesha partnered Kyosk App to provide inventory credit to merchants

IFC partnered with Orange Bank Africa to Increase Digital Lending for Small Businesses in West Africa

Online aggregator marketplace Qardy partnered with Egypt Post to offer SMEs access to financing opportunities

Digital payment company Pesapal has partnered with digital credit provider Sokohela to launch a credit product focused on SMEs.

Ethiopian fintech Chapa partnered with local banks to offer loans for small and medium-sized enterprises.

Moniepoint launched Working Capital Loans, a product that offers their Merchants short to medium-term loans ranging from 7 to 120 days.

We trust this piece was insightful.. let’s move to something else..

🥸 Micromanagement is not your thing….

That is not the reason you became a Fintech Executive.

You had a dream, a passion, and a problem you wanted to solve

Now you spend more time explaining, reviewing, correcting, and firefighting..

Instead of creating, deploying, executing, and speaking to customers.

You deserve to take back control of your time. But how?

Our acclaimed Payments360 course provides a unique immersion for beginners and intermediate entrants to the Fintech space. This market-relevant course was developed out of our understanding of the growth trajectory of the fintech industry and the infrastructure and processes that make things work.

Join Fintech Founders, and executives who now have control of their time. Classes are online, on Saturday, from 9 a.m. to 12 noon for 4 weeks. To learn more, read reviews, and download a detailed curriculum- click here:

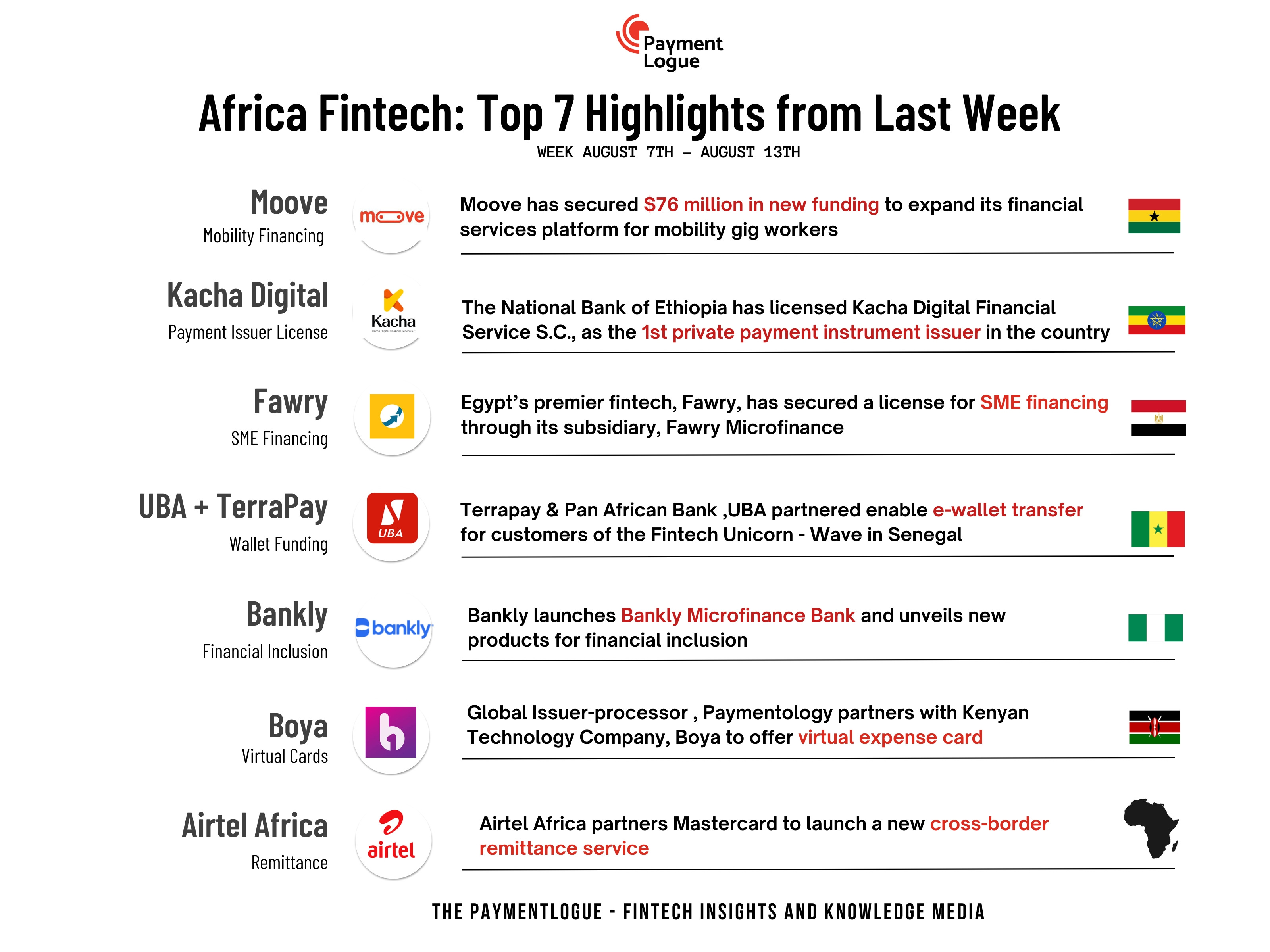

The Weekly Roundup

Finally, on today’s dashboard, we’ve selected the top 8 headlines that made the most impact, take a look 👇🏽.

And that is all for this week’s newsletter. If you found this informative, please subscribe, comment, and share in your Fintech circle. Have an awesome week!